International. The global paint and coatings market size was valued at $206.56 billion in 2023 and is projected to grow from $217.36 billion in 2024 to $303.97 billion in 2032, according to a report by Fortune Business Insights.

The automotive, construction, wood, and transportation industries frequently use paints and coatings. They are widely used in the construction industry to protect buildings from damage from the outside.

Years ago, in the midst of the pandemic, companies focused on managing orders, inventory, and shipments in transit. Companies continuously employed state-of-the-art strategies to maintain the stability of their operations at industrial plants. During the pandemic, suppliers placed a high priority on efficient logistics and distribution of raw materials. Currently, due to the expansion of the construction and automotive industries, the market is anticipated to return to its pre-pandemic level.

The Resins Market is segmented into Acrylic, Alkyd, Epoxy, Polyurethane (PU), Polyester, and Others. Due to its adhesion qualities, drying speed, relative strength, and flexibility, acrylic resin stands out from the competition and holds a substantial share in the market. This makes it ideal for use in paints and coatings.

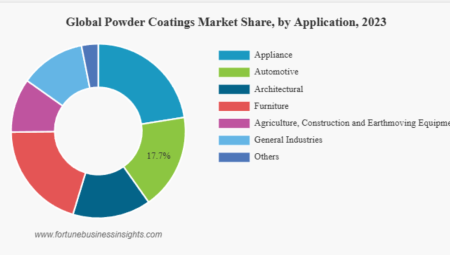

By application, the market is divided into architectural, industrial wood, marine, automotive OEM, automotive refinishing, general industries, coils, protective coatings, packaging, and others. During the projected period, the architectural segment is expected to dominate in terms of revenue and volume. Paints and coatings are primarily used for ornamental purposes in architectural applications to protect residential and non-residential structures and buildings from UV radiation, environmental damage, and other factors.

Most infrastructures and structures are protected and decorated with paints and coatings. Paints, sealants, primers, stains, and varnishes for exteriors and interiors are some examples of these architectural advances. The growth of the market is likely to be driven by an increase in construction activity and government investment in various public infrastructure projects. In addition, cutting-edge technologies are gradually becoming the norm in the construction industry. Another element driving the expansion of the construction sector is the increased use of cloud computing and collaboration, as well as building information modeling (BIM). These factors are anticipated to increase the market share.

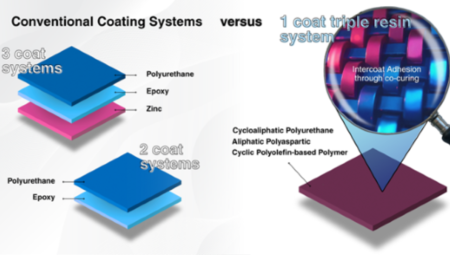

However, producing thin coatings is challenging. The speed and volume of powder applied to the substrate are difficult to regulate, which can hinder the growth of the paints and coatings market.

In terms of volume and revenue, Asia Pacific had the largest market share in paints and coatings in 2022 and is likely to maintain that position over the forecast period. This is a result of the expansion of construction and building activity, as well as the automotive industry in China, India and Japan. Due to their use to cover both residential and non-residential infrastructure, paints and coatings are in higher demand.

In order to preserve the quality of products and increase their regional presence, most multinational companies have integrated their raw material production and sales activities. As a result, businesses gain a cost advantage that increases profit margins and offers them a competitive advantage. Corporations are also placing greater emphasis on their R+D activities to stay competitive and meet the changing demands of end-users.